Decoding Data Centers: How Infrastructure Meets Real Estate

Based on CBRE Investment Management’s “Data Center Investment: Decoding Opportunities” (Tania Tsoneva & John Affleck, July 2024)

As digital infrastructure reshapes the global economy, data centers have emerged as one of the most compelling investment frontiers. According to CBRE Investment Management, these assets occupy a unique space since they are part infrastructure and part real estate, underpinned by powerful demand from AI, cloud computing, and digital services.

The Dual Identity: Infrastructure and Real Estate

CBRE frames data centers as a hybrid asset class, merging the stable characteristics of infrastructure with the tangible assets of real estate.

Infrastructure traits: They deliver an essential utility – digital interconnectivity and computation – with long-term contracts, high barriers to entry, and stable revenue.

Real estate traits: They are physical assets where land, power access, and permitting determine value, and where tenants lease space are often measured by kilowatts/megawatts rather than square feet.

This intersection means investors must evaluate both the stability of the tenant’s contract (infrastructure) and the quality and capacity of the physical facility (real estate).

Power and Technical Expertise Define Value

In a traditional office building setting, the most priced room is often one with the best view. In a data center, CBRE highlights the core commodity in this market is power, not space. Tenants, often cloud giants or telecom operators, are effectively paying for guaranteed electrical capacity and uptime. High availability is crucial, so tenants will pay a premium price for facilities that can deliver “five nines” (99.999%) of uptime.

These clients demand technical excellence, redundancy, security, and efficient cooling. This makes operational expertise a critical differentiator for developers and owners. For investors, this means the value of a data center isn’t just in its land or building, but in the quality of its engineering and the expertise of its operators. A well-run facility with superior technical specs can command higher rents and retain tenants longer, making operational prowess a direct driver of financial returns.

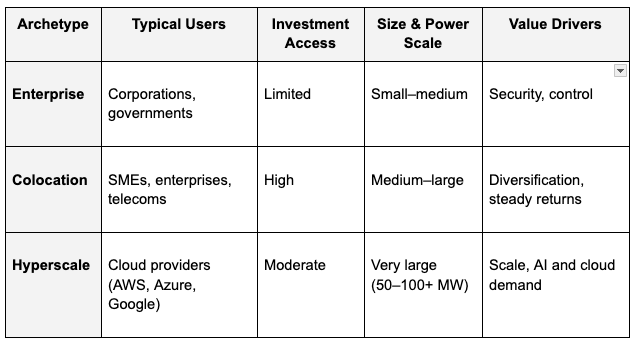

The Three Data Center Archetypes

CBRE outlines three main models shaping the market:

Enterprise Centers: These facilities are owned and operated by corporations for internal workloads and are off-limits to outside investors. Typical users include financial institutions, healthcare providers, and government agencies that require strict control over data and security.

Colocation Centers: Shared facilities rented by multiple tenants. Retail colocation offers racks and cabinets; wholesale leases entire suites for 5–20 years. Their diversified tenant mix and recurring revenue streams make them highly attractive to institutional investors seeking stable, utility-like income.

Hyperscale Centers: Massive, custom-built sites for major cloud providers with stringent technical and security requirements. Users are global providers like Amazon, Microsoft and Google

Nearly 900 hyperscale facilities now exist globally, which is 37% of total capacity. Furthermore, that share could approach 50% by 2027 as enterprises migrate away from on-prem systems. Leasing is accelerating too: hyperscale’s ownership mix has shifted from 50:50 (own vs. lease) to roughly 70:30 in favor of leasing, expanding third-party investment opportunities.

Demand-Supply Imbalance: The Power Conundrum

Despite record levels of construction, the article notes that global data center demand continues to far outpace supply.

Demand drivers:

Explosive data creation across IoT, 5G, and AI ecosystems.

Generative AI workloads requiring greater density and power per rack.

Supply bottlenecks:

Power scarcity: Securing grid connections can take up to 15 years.

Permitting and land constraints: Only select sites can accommodate cooling, redundancy, and zoning requirements.

Construction inflation: Rising CapEx that is up to $10–14 million per MW is limiting new entrants.

Even as 70 million square feet of capacity is in development, CBRE reports vacancies below 1% in markets like Northern Virginia, reinforcing long-term pricing strength.

Investment Approaches and Risk Profiles

CBRE identifies three main routes into the data center market, each representing a different balance of risk, control, and required expertise. Choosing the right path is less about finding the “best” option and more about finding the right fit for an investor’s capital, capability, and conviction.

Direct Acquisitions: Here, lower execution risk but intense competition and potential obsolescence. This approach involves buying an existing, operational facility. It’s the real estate equivalent of buying a tenanted office building.

Development Projects: High CapEx but strong control and customization potential. It entails building a new data center from the ground up, offering maximum control over the final product.

Platform Investments: Equity stakes in operators provide scale and diversification but at elevated valuations that are often 25–30× EV/EBITDA. Instead of buying a single asset, this means taking an equity stake in the operating company that builds and manages a portfolio of data centers.

Choosing between them depends on capital structure, expertise, and risk appetite.

Key Risks on the Horizon

Beyond the risks inherent to each investment route above, the article identifies systemic challenges that threaten the entire sector’s growth and profitability.

Technological Obsolescence: Rapid evolution in chips, cooling, and architecture.

Grid Limitations: Energy shortages could cap expansion.

ESG Pressure: Sustainability mandates are intensifying scrutiny.

Valuation Risk: Premium pricing may compress as capital floods in.

CBRE emphasizes that aligning with experienced operators and prioritizing sites with reliable renewable energy access can mitigate many of these risks.

The Broader Implication

The report underscores a paradigm shift: data centers are no longer just warehouses for servers, they are the backbone of modern economies. In a world increasingly defined by AI and digital transactions, power capacity has become the new land, and compute the new currency.

References

CBRE Investment Management. “Data Center Investment: Decoding Opportunities.” Authors: Tania Tsoneva and John Affleck. Published July 17, 2024. Available at: https://www.cbreim.com/insights/articles/decoding-data-centers

The framing of data centers as a hybrid asset class is insightful. Most people overlook that power reliability and operational excelence are the real differentiators now, not just land costs. With AI driving exponential demand, the companies that can guarentee uptime and cool efficiency will dominate the market. This shifts how we should evaluate infrastructure investments going forward.